News

Do you know your Pension Lifetime Allowance? - Part 2

PART 2 -WHAT HAPPENS TO PENSION FUNDS IN EXCESS OF THE LIFETIME ALLOWANCE? AND WHAT HAPPENS ON YOUR DEATH?

In the last edition of this four-part series on the pension Lifetime Allowance, Richard Wadsworth, Director, Glasgow, reviewed the basics of the LTA: What it is?

How do you measure your funds against it? And when is the best time to do so?

In Part Two, we now consider the

excess funds remaining beyond

the LTA. How are these taxed?

And also, what happens upon

your death?

PENSION LIFETIME ALLOWANCE (LTA)

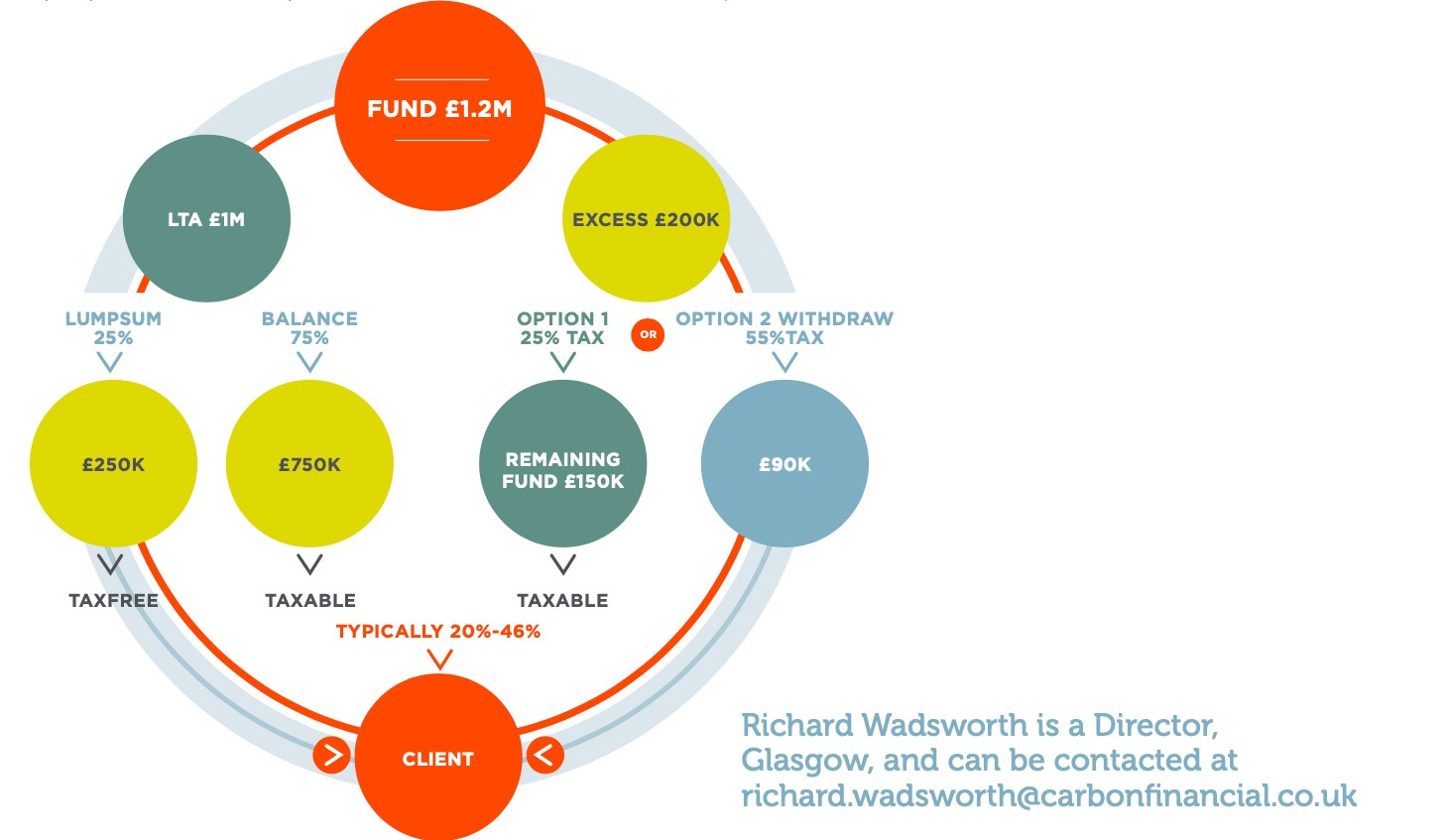

What is the rate of tax I would pay on the excess?

Broadly speaking, 25% is the additional tax you pay on that amount which exceeds the LTA.

-

So, if, for simplicity, the LTA was £1m and your funds were worth £1.2m, the tax charge would be 25% of £200k = £50,000.

-

You would then have £1,150k of funds to draw on.

-

Of the £1m that falls within the LTA, 25% (£250,000) can be taken as tax-free cash, with income tax falling due on the remaining £750,000 as and when it is paid out, and at your relevant rate, typically 20% to 46%, depending on how much income you have and whether you live in Scotland or the rest of the UK. (As this is pension income, no National Insurance deductions are made).

Of the remaining £150,000 net of the LTA tax charge, no tax-free cash can be taken, and the full £150,000 would be liable to income tax as and when it is paid out – so the effective LTA excess tax rate is arguably a little more than 25% because you will pay income tax on the full amount with no tax-free element.

Is there any alternative to paying the 25% tax rate?

Yes. As an alternative to paying 25% of the excess and then income tax, you can opt for a combined tax rate of 55%. The rate that works out best for you will depend on your prospective income tax position.

If you are expected to pay less than 40%, you would be better paying the 25% tax rate, then the income tax.

The rate is 25% at age 75 on any funds not already taken, or any growth on funds since they were moved into drawdown and then income tax would be liable on funds drawn in the same way as noted above.

In all cases the tax charge would be paid from pension funds so its effective cost is arguably reduced, as it is paid from funds which have received tax relief.

What rate of tax would be paid on my death?

Upon death, the rate of tax on the excess over the LTA, but only if the funds pass to a beneficiary’s pension. In other words, the funds go from one pension pot to another. When income is subsequently drawn from the beneficiary’s pension, it may be subject to income tax.

If, instead of the funds being passed to a beneficiary’s pension, the pension fund is paid out on death, 55% is applied to any excess over the LTA.

Again, the tax charge would be paid from pension funds, so its

effective cost is arguably reduced as it is paid from funds which

have received tax relief.

A downloadable PDF of this article is available, here

We hope you’re still with us – there’s a lot to think about! But the more you know, the more likely you are to ask the right questions

and make good decisions. In our next piece, Part Three of this series ,we take a look at two more questions which are often asked:

what happens if you don’t expect to take your pension benefits all at the same time? And what are the implications of moving funds

into drawdown?

The value of investments and the income derived from them can fall as well as rise. You may not get back what you invest. This communication is for general information only and is not intended to be individual advice. It represents our understanding of law and HM Revenue & Customs practice. You are recommended to seek competent professional advice before taking any action. Tax and Estate Planning Services are not regulated by the Financial Conduct Authority.

Sign-up for our Carbon Catch-Up Newsletter

Part of The Progeny Group

Progeny is independent financial planning, investment management, tax services, property, HR and legal counsel, all in one place.

Carbon Financial Partners, part of The Progeny Group, is a trading name of Carbon Financial Partners Limited which is authorised and regulated by the Financial Conduct Authority under reference 536900.

Carbon Financial Partners Limited is registered in Scotland. Company registration number SC386400. Registered Address: 61 Manor Place, Edinburgh, EH3 7EG. Carbon Financial Partners Limited is part of The Progeny Group Limited.

© Carbon Financial Partners 2026

www.financial-ombudsman.org.uk

Client Account | Personal Finance Portal | Privacy Notice | Cookies | Careers